No. 076 – Find the sweet spot between risk and reward on every investment

Question

I am worried about my investments. My local investments are down by 10% and my offshore ones by almost 20%. I am considering taking my money out and keeping it in the bank until the financial crisis is over. Is this a good strategy?

Answer

The investment market has been very volatile because of the war in Ukraine and China’s Covid lockdowns, which caused supply chain disruptions. Add in the impact of central banks trying to curb inflation and you have a perfect storm. All the markets are down and most of us have felt like doing what you are considering.

Every investment is a combination of risk and reward. If there is no risk, there is little reward but if there is high risk, there is the potential of a high reward. The challenge for all investors is to find that sweet spot.

If you are a conservative investor, you can leave all your money in the bank where you are guaranteed that your capital will not decrease. The challenge, however, is that over time the interest that you get will not always keep up with inflation and you could find yourself getting poorer over the years. I regularly assist people in their 70s who are in this situation. They have invested their money in conservative investments and are finding it extremely difficult to come out on their income.

It comes to investing, the key factor is time and I will explain why.

Share prices move up and down all the time. Sometimes these movements are quite large. However, over time, the overall movement of the investment market is positive. Now, if you are using the investment to pay for something in the very near future or use it to provide an income, you cannot afford to be in a situation when you are drawing out funds when the market is down. You need to keep these funds in an investment that does not move up and down that much.

On the other hand, if your investment will only be needed many years from now, you will be in a much better situation if you had some exposure to the share market.

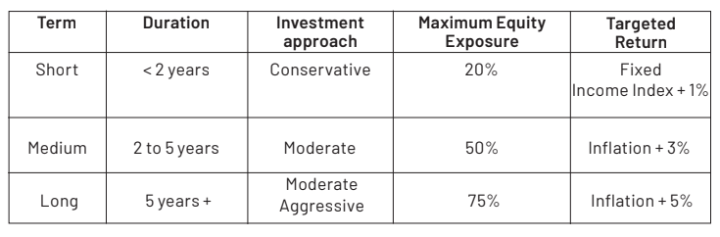

I like split investments into three pots depending on when you plan to access the funds:

There will be times when the markets are down (like now) but if you have a short-term goal, you should not have more than 20% of your investment in the stock market so the impact should be limited. If you have a longer-term need, don’t worry, the markets should bounce back over time.

So, to answer your question, do not cash in your investments now if you can help it – you will just lock in the losses.

It is impossible to time the market and know when to get back in. The market often overreacts to bad news and when things recover, the bounce-backs are often sudden and high.

If you were out of the market for the best five days in the past 22 years (which is more than 8,300 days), your returns would have been 28% less than they could have been. This amount increases to 78% if you were out for the best 30 days.

Time in the market beats timing the market.

KENNY MEIRING IS AN INDEPENDENT FINANCIAL ADVISER

Contact him via phone, email or via contact phone on the financialwellnesscoach.co.za website

Read more of our articles on the Daily Maverick website or newspaper weekly!

adminfwc

adminfwc

No. 264 – Turning property proceeds into a tax-efficient retirement income

adminfwc

No. 263 – How to plan for your pets’ care after your death

adminfwc

No. 262 – Planning is crucial in turning a business into usable family capital

adminfwc

No. 261 – Pay your future self first when you’re earning well

adminfwc

No. 260 – The taxes and fees to consider for estate planning

adminfwc

No. 259 – Plan and save now to fund cost of assisted living

adminfwc

No. 258 – Resigning shortly before retiring: several factors to keep in mind

adminfwc

No. 257 – Managing financial affairs after a loved one dies

adminfwc

No. 256 – The numbers behind a university flat investment

adminfwc