No. 071 – Consider the pros and cons of life and living annuities

Question

I retired three years ago, with half my income coming from my company pension fund and the other half from interest from investments. I am paying tax at a rate of 41%. Is there anything that I can do to reduce this amount?

Answer

When you retire, there are several instruments that you can use to provide an income. Most people use only a living annuity, but it is rare that just one of these instruments meets a person’s needs optimally. The aim here is to receive a sustainable retirement income, pay as little income tax as possible and not lose money in the form of estate duty when you die. Most of my retirement income solutions use a combination of living annuities, life annuities and drawdowns from discretionary investments.

Over the past few years, low interest rates and decent bond yields have resulted in annuity rates being extremely attractive and offering good value for money. I have used them to secure decent incomes for pensioners who were drawing down too much on their living annuities.

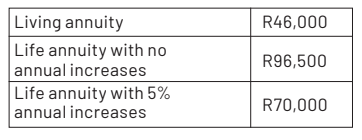

Let me give you a sense of the difference in income that you can get by adding a life annuity into your investment mix. The recommended drawdown rate for a 76-year-old is 5.5%. Your R10-million living annuity would thus give you a sustainable income of about R46,000 a month.

A life annuity, on the other hand, would pay out a level amount of R96,500 a month for the rest of your life and your wife’s life. If you wanted an annuity that increased by 5% a year, the annuity would start off at R70,000 a month.

To summarise, we have:

As you can see, the life annuity will provide a much higher income for you. There are a few reasons this is the case:

- As life annuities are provided by life insurance companies, they make use of life expectancy tables. The people who live beyond the life expectancy level are subsidised by those who die early. When you have a living annuity, you have to invest as though you are going to live to 100, as you cannot afford to run out of money.

- Life insurance companies can afford to be a little more aggressive about how they invest the money, as they have large pools to invest. As an individual, you cannot afford to take a chance with your retirement capital, so you need to invest more conservatively and give up some potential growth.

Downside of life annuities

Life annuities are designed to provide you with a pension for the rest of your life. Once they are set up, there is very little flexibility. You lock yourself into a particular income stream and that will be paid to you for the rest of your life.

The other weakness of the annuity is that it is not designed to pay an inheritance. With the living annuity, there will often be an amount that your children can inherit once you and your spouse have died.

This is not the case with a life annuity, as your children will stand a much lower chance of inheriting because your pension will have dried up.

I like to use a life annuity in conjunction with a living annuity. The life annuity is used to cover your fixed costs such as your utility bills and medical aid, and the living annuity covers the rest.

In the example below, if you bought a life annuity of R3-million and used R7-million to make up the balance of your income, you could significantly reduce your living annuity drawdown rate:

Having a lower drawdown rate can increase the chances of the capital value of your living annuity increasing over time. Not only will this give you greater financial security, you will also increase the chances of your children inheriting something once you and your spouse have died.

Converting your retirement assets into an income should not be done lightly.

I would recommend that you chat to a financial adviser, who can advise you on the right combination of life and living annuities.

KENNY MEIRING IS AN INDEPENDENT FINANCIAL ADVISER

Contact him via phone, email or via contact phone on the financialwellnesscoach.co.za website

Read more of our articles on the Daily Maverick website or newspaper weekly!

adminfwc

adminfwc

No. 264 – Turning property proceeds into a tax-efficient retirement income

adminfwc

No. 263 – How to plan for your pets’ care after your death

adminfwc

No. 262 – Planning is crucial in turning a business into usable family capital

adminfwc

No. 261 – Pay your future self first when you’re earning well

adminfwc

No. 260 – The taxes and fees to consider for estate planning

adminfwc

No. 259 – Plan and save now to fund cost of assisted living

adminfwc

No. 258 – Resigning shortly before retiring: several factors to keep in mind

adminfwc

No. 257 – Managing financial affairs after a loved one dies

adminfwc

No. 256 – The numbers behind a university flat investment

adminfwc