No. 061 – How to manage a retirement annuity pay out

Question

I retired three years ago, with half my income coming from my company pension fund and the other half from interest from investments. I am paying tax at a rate of 41%. Is there anything that I can do to reduce this amount?

Answer

There are a few things you need to look at before you go down this path.

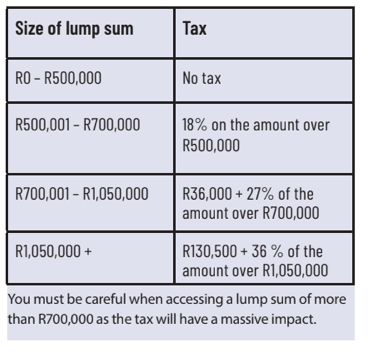

Tax

The tax on your retirement lump sums works on a sliding scale. The more you withdraw, the bigger the portion you pay to the Receiver.

Income

The rest of your retirement benefit must be used to generate an income. Be careful about letting this become part of your household income while you are still working. I would recommend you take this money annually and invest it so you are not tempted to use it.

Risk

By investing your retirement savings in your business, you are putting all your eggs in one basket. If the business succeeds, you are fine; if it run into difficulties, you could be in trouble.

By investing your retirement savings in your business, you are putting all your eggs in one basket. If the business succeeds, you are fine; if it run into difficulties, you could be in trouble.

Estate planning

In essence, your retirement savings do not form part of your estate. This means that the value of your retirement annuities or living annuities may be passed on to your heirs without paying 20% estate duty. By taking money out of retirement savings and putting it into your bond you are reducing the size of your assets that fall out of the estate duty net.

Longevity of the business

You need to give serious thought to this. I regularly see clients with their own businesses who are looking to retire (or reduce their involvement in the business). The challenge is that they might not have strong enough staff to run the business when they are not involved.

If you are going to put part of your retirement savings at risk by investing in the business, you need to ensure the business is sustainable when your involvement is cut back.

The business must be correctly structured so you can do one of two things:

- Sell it and use the proceeds to provide you with an income for the rest of your life; or

- Use it to draw an ongoing income till you and your spouse die.

There are people who specialise in helping small business owners do this.

You need to get your business valued by a specialist. Many small business owners massively underestimate the value of their business. This can cause problems when sorting out the estate, as there is often not enough liquidity to pay various taxes.

Once you appreciate the value of the business, you can put structures in place to attract the right calibre of staff. This will improve your chances of selling the business for a decent price. Or you will ensure that the business carries on running at the level it was when you were still actively involved.

There are several clever financial structures that small businesses could use to:

- Attract and retain key staff;

- Help the next generation of leadership buy into the business; and

- Extract value when you retire.

Chat to an experienced financial adviser who can unpack the issues and help you to make the right decision.

KENNY MEIRING IS AN INDEPENDENT FINANCIAL ADVISER

Contact him via phone, email or via contact phone on the financialwellnesscoach.co.za website

Read more of our articles on the Daily Maverick website or newspaper weekly!

adminfwc

adminfwc

No. 262 – Planning is crucial in turning a business inito usable familty capital

adminfwc

No. 261 – Pay your future self first when you’re earning well

adminfwc

No. 260 – The taxes and fees to consider for estate planning

adminfwc

No. 259 – Plan and save now to fund cost of assisted living

adminfwc

No. 258 – Resigning shortly before retiring: several factors to keep in mind

adminfwc

No. 257 – Managing financial affairs after a loved one dies

adminfwc

No. 256 – The numbers behind a university flat investment

adminfwc

No. 255 – Don’t let short-term panic derail long-term plans

adminfwc

No. 254 – How you can protect your finances when faced with retrenchment

adminfwc