No. 080 – How to navigate living annuities, drawdown rates and volatile markets

Question

I retired three years ago, with half my income coming from my company pension fund and the other half from interest from investments. I am paying tax at a rate of 41%. Is there anything that I can do to reduce this amount?

Answer

When you take out a living annuity and set your drawdown rate at, say, 5%, the product supplier will calculate the drawdown at the start of the period and then divide it into 12 equal payments to give you the same pension each month.

If the markets fall during the course of the year, your actual drawdown could be more than 5% in a particular month.

A typical living annuity will cost about 3% a year to run and if you are drawing down 5% as an income, then your investment needs to return 8% a year so that you do not start drawing into your capital.

Now, the first six months of this year were not good for investors and the stock markets fell by about 10%. If you had picked your investment portfolios badly, then you could be in trouble.

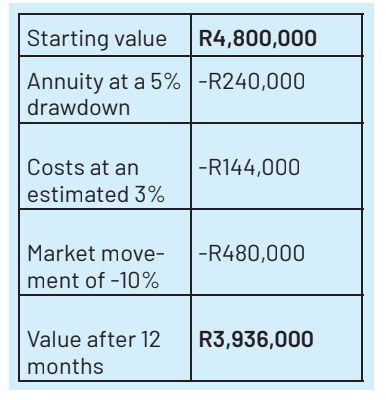

For example, if you took out a living annuity for R4.8-million with a 5% drawdown (which would give you R20,000 each month) and the stock market fell by 10% over the course of the year, the capital in your living annuity would drop to just under R4-million after a year.

In order to keep the same income of R20,000 a month, you would have to increase your drawdown percentage to 6.1%.

If you wanted to increase your monthly income by 6% to keep up with inflation, your drawdown rate would have to increase to 6.5%. You are rapidly moving into the zone where you are living off your capital rather than your investment income.

What can you do?

There are a few things you can do to improve the situation:

Invest in portfolios with downside protection

There are portfolios that use financial structures to limit any downwards market movement. These include guaranteed funds, funds with high watermark guarantees, absolute return funds and real return funds.

There is an additional cost to these but under the current circumstances they are worth considering.

Structure your living annuity portfolio with care

I like to keep two years’ income in a low-risk portfolio and draw the monthly income from it. This will ensure that you do not have to sell equities when the market is doing badly. Keep the rest of your funds in longer-term growth assets.

Use some of your retirement savings to buy a life annuity

A recent change in legislation allows you to buy both a life and a living annuity with the proceeds of your retirement savings. Life annuity rates are good at the moment and by using a portion of your investment to buy a life annuity you can significantly reduce your living annuity drawdown rate.

KENNY MEIRING IS AN INDEPENDENT FINANCIAL ADVISER

Contact him via phone, email or via contact phone on the financialwellnesscoach.co.za website

Read more of our articles on the Daily Maverick website or newspaper weekly!

adminfwc

adminfwc

No. 264 – Turning property proceeds into a tax-efficient retirement income

adminfwc

No. 263 – How to plan for your pets’ care after your death

adminfwc

No. 262 – Planning is crucial in turning a business into usable family capital

adminfwc

No. 261 – Pay your future self first when you’re earning well

adminfwc

No. 260 – The taxes and fees to consider for estate planning

adminfwc

No. 259 – Plan and save now to fund cost of assisted living

adminfwc

No. 258 – Resigning shortly before retiring: several factors to keep in mind

adminfwc

No. 257 – Managing financial affairs after a loved one dies

adminfwc

No. 256 – The numbers behind a university flat investment

adminfwc