No. 092 – The implications of what used to be called ‘financial emigration’

Question

I have been living in Australia for the past five years and have just been granted permanent residence status. I want to emigrate financially and would like to know what the implications are. My only asset in South Africa is a R1.6-million preservation fund.

Answer

Financial emigration has been replaced by the concept of being “ordinarily resident” in a country. This is a fairly loose term, but it boils down to which country is the place that you actually call home now. As you have been living in Australia for the past five years, it would be safe to say that you would pass the test of being ordinarily resident in Australia.

When you notify the SA Revenue Service (SARS) that you are ordinarily resident in Australia, it will trigger a capital gains tax (CGT) event. As your only asset is your preservation fund, CGT will not be an issue. However, if you had other investments in South Africa, CGT would have to be paid, even if you had not sold them.

What to do with the retirement fund

As South African retirement products can only be transferred to other retirement funds registered within South Africa, you cannot transfer your preservation fund to a retirement fund in Australia. You must either withdraw the proceeds or retire from the fund.

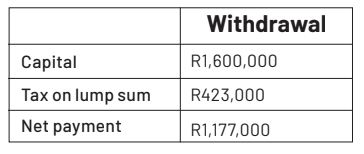

Withdrawal of proceeds

Your money is in a preservation fund. You are allowed to make one withdrawal from it. If you have not made that withdrawal before, you may withdraw the full value of this preservation fund and transfer it to Australia.

If you have made a prior withdrawal, you may withdraw the proceeds from the preservation fund if you have not been resident in South Africa for an uninterrupted period of three years. The withdrawal will be subject to tax as per the withdrawal benefit table.

You will get the following if you withdraw:

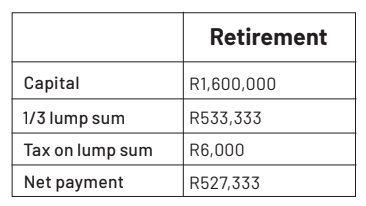

Retiring from the preservation fund

You may retire from the fund from the age of 55. You can take one-third of the investment out as a lump sum and have the balance paid out as an annuity. Your lump sum would be:

In addition to this, you will have an amount of R1,072,667 that must be used to buy an annuity.

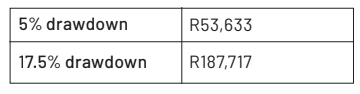

Now, depending on your broader financial plan, you may want to use the South African investment to provide diversity to your investment portfolio. You would use an annuity drawdown rate of 5%. If you want to get your funds out of South Africa as quickly as possible, you can drawdown at 17.5% and exhaust the capital within a couple of years.

I usually recommend to my clients that they have the annuity paid annually as it is just simpler to transfer the funds overseas. This is what the annual annuities would look like:

This is just a brief overview of a complex issue and I would recommend that you speak to a professional who specialises in emigration before you make any big decisions.

KENNY MEIRING IS AN INDEPENDENT FINANCIAL ADVISER

Contact him via phone, email or via contact phone on the financialwellnesscoach.co.za website

Read more of our articles on the Daily Maverick website or newspaper weekly!

adminfwc

adminfwc

No. 264 – Turning property proceeds into a tax-efficient retirement income

adminfwc

No. 263 – How to plan for your pets’ care after your death

adminfwc

No. 262 – Planning is crucial in turning a business into usable family capital

adminfwc

No. 261 – Pay your future self first when you’re earning well

adminfwc

No. 260 – The taxes and fees to consider for estate planning

adminfwc

No. 259 – Plan and save now to fund cost of assisted living

adminfwc

No. 258 – Resigning shortly before retiring: several factors to keep in mind

adminfwc

No. 257 – Managing financial affairs after a loved one dies

adminfwc

No. 256 – The numbers behind a university flat investment

adminfwc